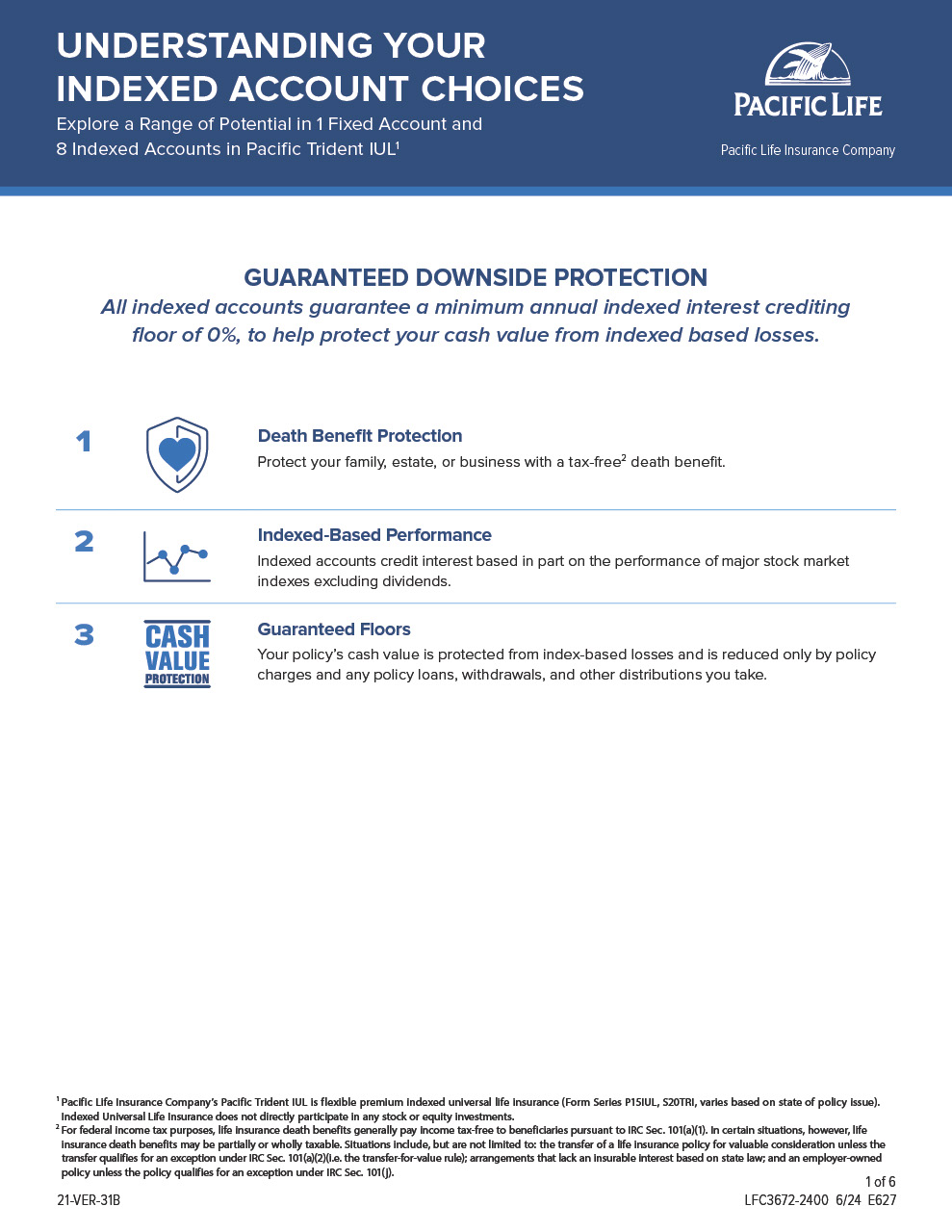

Death Benefit Protection with Competitive Guarantees and Flexible Choices

Pacific Trident IUL

Indexed Universal Life Insurance 1

Key Features

Tax-free3 death benefit helps provide financial protection for your client’s family, business, or estate.

Guaranteed minimum cash surrender values,4,5 interest crediting rates, no-lapse protection,4,6 and a 1% interest guarantee on termination4,7 to help your client mitigate interest crediting risk.

Flexible choices in indexed accounts, policy access options, and optional riders for long-term care4,8 or chronic illness protection.4,9

Help your business and high-income clients achieve their accumulation goals. Request your product marketing kit now.

Connect with us to learn what Pacific Trident IUL can do to help your clients looking for competitive guarantees and cash value accumulation potential.

Firm and state variations may apply. Contact your Pacific Life representative for availability.

Life insurance is subject to underwriting and approval of the application and will incur policy charges.

1Form series P15IUL, S20TRI, varies based on state of policy issue. Indexed universal life insurance does not directly participate in any stock or equity investments.

2Product’s issue ages are 0-90.

3For federal income tax purposes, life insurance death benefits generally pay income tax-free to beneficiaries pursuant to IRC Sec. 101(a)(1). In certain situations, however, life insurance death benefits may be partially or wholly taxable. Situations include, but are not limited to: the transfer of a life insurance policy for valuable consideration unless the transfer qualifies for an exception under IRC Sec. 101(a)(2)(i.e. the transfer-for-value rule); arrangements that lack an insurable interest based on state law; and an employer-owned policy unless the policy qualifies for an exception under IRC Sec. 101(j).

4Riders will likely incur additional charges and are subject to availability, restrictions, and limitations. Clients should be shown policy illustrations with and without riders to help show the rider’s impact on the policy’s values.

5Limited Return of Premium Guarantee Rider (Form #R20ROP, varies based on state of policy issue).

6The No-Lapse Guarantee Rider (Form series R17FNL, S18FNL, varies based on state of policy issue), depending on how your client structures their policy, has a maximum duration of the insured’s lifetime, subject to certain limits. If your client’s net no-lapse guarantee value is zero, the no-lapse feature terminates. If the no-lapse feature terminates, additional premiums would be required to resume the no-lapse guarantee. If policy performance is such that your client’s policy is being maintained solely by the no-lapse guarantee, your client’s policy will not build cash value.

7The Interest Guarantee on Termination Rider (Form #R20IGT, varies based on state of policy issue) is issued with the policy at no additional cost.

8Premier LTC Rider (Form series R15LTC, R15LTC SP, varies based on state of policy issue) is an Accelerated Death Benefit Rider for Long-Term Care.

9Premier Living Benefits Rider 2 (Form series R18ADB, S18ADB, varies based on state of policy issue). There is no up-front cost or monthly rider charge for the Premier Living Benefits Rider 2. The cost of exercising the rider is that the death benefit is reduced by an amount greater than the rider benefit payment itself to reflect the early payment of the death benefit. Benefits paid by accelerating the policy’s death benefit may or may not qualify for favorable tax treatment under Section 101(g) of the Internal Revenue Code of 1986.